Liquor baron Vijay Mallya (60) and his Rs 7,000-crore default occupy headlines, but there are 5,275 other “wilful defaulters”—together, they owe India’s banks Rs 56,521 crore ($ 83.9 billion), according to the Credit Information Bureau (India), or CIBIL, a company set up by banks to collect defaulter information.

The money that wilful defaulters owe Indian banks has grown nine-fold over 13 years, and is more than 1.5 times the Central government’s allocation for agriculture and farmer welfare (Rs 35,984 crore) in Union Budget 2016-17, according to an IndiaSpend analysis of CIBIL data.

Banks declare borrowers to be “wilful defaulters” when they deliberately do not repay loans, despite the ability to do so. Many defaults may not be wilful, caused as they may be by adverse economic conditions.

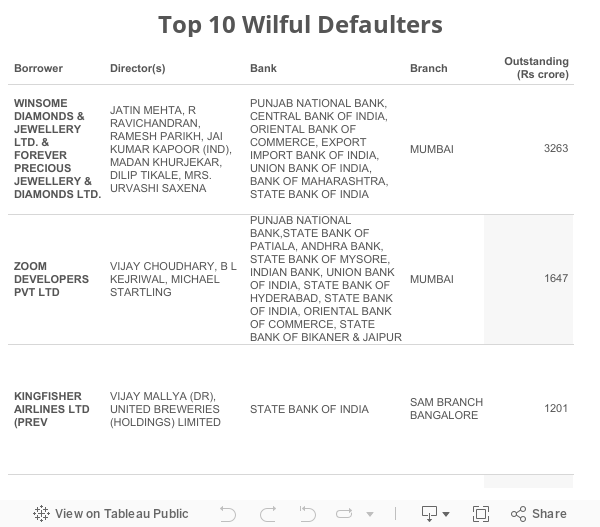

India’s five leading wilful defaulters (the following figures are the single-biggest loan and not the collective sum owed):

- Mumbai-based Winsome Diamonds & Jewellery and associate Forever Precious Jewellery & Diamonds,: Rs 3,263 crore

- Indore-based real-estate developer Zoom Developers: Rs 1,647 crore

- Kingfisher Airlines: Rs 1,200 crore

- Mumbai-based Beta Naphthol: Rs 951 crore

- Kanpur-based Raza Textiles: Rs 694 crore

Except Winsome Diamonds & Jewellery, the other companies are in various stages of liquidation, according to the Ministry of Corporate Affairs website. E-mails sent last week to Winsome Diamonds and Kingfisher Airlines went unanswered, as did emails to two prominent banks that loaned them money—State Bank of India (SBI) and Punjab National Bank (PNB).

Amount Owed by Wilful Defaulters Grows Nine-fold Over 13 Years

In 2002, the total amount owed by wilful defaulters was Rs 6,291 crore ($9.3 billion). It grew—as we said—nine-fold over the next 13 years to Rs 56,521 crore ($83.9 billion).

A powerful nexus between chairmen of public sector banks, auditors, Reserve Bank of India and the banks’ boards is behind the country’s total Non-Performing Assets (NPA) and wilful defaultersS Nagarajan, General Secretary, All India Bank Officers’ Associations.

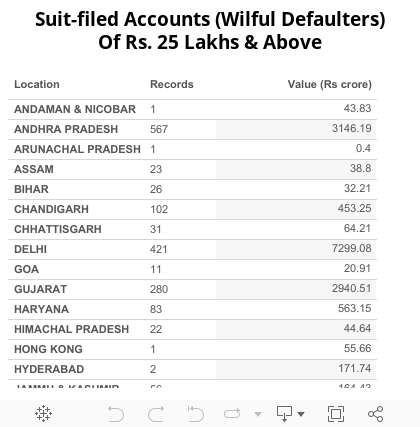

Maharashtra has more wilful defaulters than any other state: 1,138, who owe Rs 21,647 crore. Next is West Bengal with 710 and Andhra Pradesh with 567 cases. But in terms of defaults, Delhi is second with more than Rs 7,299 crore.

Speaking on condition of anonymity, a senior executive manager of a Singapore-based bank said: “Often, banks do not even report unpaid loans to CIBIL due to a nexus between politician and defaulter. Kingfisher is on the list because Mallya’s cover has been blown. This is the reason corporate get easy loans from government banks and not private and foreign banks.”

Private-sector banks also have an unpaid-loan problem, but their bad loans are less than half the level of public-sector banks, which account for 73 percent of all lending, as IndiaSpend reported last month.

Government banks face immense pressure from parliamentarians to provide loans to corporate, the politician-bureaucrat-corporate nexus is very strongSanat Dutta, a lawyer for nationalised banks in debt recovery tribunals for more than 10 years.

Diamonds in Dubai, Land in US, Cricket Team—What Defaulters Did With Their Loans

India’s wilful defaulters have a history of using loans from public banks for a variety of purposes–some unrelated to their businesses, others used for expansion without business diligence.

Among the wilful defaulters is English daily Deccan Chronicle, which survives despite a string of unpaid loans—used for other businesses, including a cricket team—and Mumbai-based JB Diamonds, the target of income-tax raids after a 2010 Rs 800-crore default.

Once India’s largest diamond exporter, 49-year-old JB Diamonds was accused by a Hong Kong banking administrator—the company owes Rs 500 crore to Hong Kong banks—of “well-planned fraudulent transactions”.

Jatin Mehta—promoter of India’s largest wilful defaulters, Winsome Diamonds and associate Forever Precious—was accused in forensic audits (quoted here in the Indian Express) of “wrongly attempting to distance himself” from business partners who did not pay dues, in particular a Jordanian in Dubai, but had been chosen by Mehta himself.

Vijay Choudhury, the promoter of Zoom Developers, which owes money to a consortium of 26 public-sector banks led by PNB, bought land valued at Rs 1,000 crore in the US using loan money, according to the Enforcement Directorate, which ordered the land attached. “The accused have knowingly formed various trust and beneficiary companies and projected them as independent entities concealing the relationship between the trust and the foreign companies…”, said the attachment order, quoted in India Today.

With Mallya’s Kingfisher Airlines, SBI alleged that money loaned was diverted several times to various companies of Mallya’s United Breweries (UB) group. Mallya and his company (UB Group) are contesting SBI’s charges, and the case is currently with the Bombay High Court.

Various cases are underway against wilful defaulters in debt recovery tribunals nationwide. There are many more who have escaped legal action.

More Wilful Defaulters Than CIBIL’s Data Show

CIBIL is one of four Credit Information Companies (CICs) that collect and maintain data of wilful defaulters who owe Rs. 25 lakh and more. The three other CICs are Experian Credit Information Company of India, Equifax Credit Information Services and High Mark Credit Information Services.

This CIBIL list contains data on wilful defaulters—who owe Rs 25 lakh and more and against whom suits were filed—provided by 50 of about 90 Indian banks, as on 31 December 2015. The list of defaulters held by three other CICs is here: Equifax, Experian and CRIF.

The full list of wilful defaulters is with the Reserve Bank of India (RBI), which does not disclose names. Last month, the Supreme Court asked the RBI for a list of defaulters who own more than Rs 500 crore to banks.

The RBI list contains the names of those against whom loan-recovery suits have been filed, as well as those free of legal action. As many as 7,265 borrowers (who borrowed more than Rs 25 lakh) owed Rs 64,434 crore to public-sector banks as on September 30, 2015, according to this statement in the Lok Sabha, the lower house of parliament. Of these, first-information reports—the first legal step–have been filed in only 1,624 cases.

Other than wilful defaulters, there are 7,436 others who owe banks Rs 115,301 crore ($ 171 billion), according to the CIBIL list. There are more defaulters, as we said earlier, than the CIBIL list shows.

If the unpaid loans made by India’s public-sector banks were recovered, they would be enough to pay for India’s 2015 spending on defence, education, highways, and health, as IndiaSpend reported last month. These bad loans, or gross non-performing assets (NPAs) as they are called in banking parlance, of public-sector banks have crossed Rs 4.04 lakh crore ($59 billion), a rise of 450% since March 2011.

Mallya’s Kingfisher is now the public face of a long-festering problem, but even that has been evident to those in banking circles.

After Kingfisher, the Cleanup Begins

In 2010, Kingfisher Airlines got Rs 6,900 crore from 17 lenders, mostly public-sector banks. The biggest lender is SBI with Rs 1,600 crore.

Other banks that lent money to Kingfisher include Punjab National Bank and IDBI Bank (Rs 800 crore each), Bank of India (Rs 650 crore), Bank of Baroda (Rs 550 crore), Central Bank of India (Rs 410 crore).

With the spike in loan write-offs and NPAs and a fall in profits spooking the banking sector, RBI governor Raghuram Rajan has made it clear that banks “may require deep surgery” to clean up their balance sheets and put stressed projects back on track.

One suggestion to tighten things comes from lawyer Dutta, who said the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002, needed amendment. “Currently we can’t initiate criminal proceedings against the defaulters as the act is civil in nature,” he said.

(Himadri Ghosh, the author, is with 101reporters.com, a pan-India network of grassroot journalists. He writes on political and social impact stories.)