The Indian rupee hit its all-time low of 68.86 against the US dollar in trade on Thursday. It’s possible that in the coming days, the rupee will fall below those levels, with some currency strategists suggesting that new lows between 69-70 against the US dollar are very possible.

A fall to new lows, however, should not be seen a negative. Unlike in 2013, the rupee’s weakness is largely being driven by global factors like the rise in US bond yields and the surge in the US dollar. Both factors are weighing on emerging currencies across the board. In 2013, the Indian rupee, along with the currencies of fundamentally weak economies, had seen a steeper sell-off compared to many other currencies. This time, the rupee’s performance is better than many other emerging market peers.

In fact, going by some indicators, like the real effective exchange rate (REER), a depreciation of the rupee is actually a good thing.

Rupee Is Overvalued

As the chart below shows, while the spot rupee rate may be close to levels seen in 2013, the 36-country trade weighted REER is actually far higher than in 2013. Over the last three years, a steady flow of foreign inflows has kept the rupee steady while currencies of trading partners have depreciated.

This has led to an overvaluation of the currency. The 36-country REER is, in fact, at a historical high and a correction in this overvaluation would be beneficial for exporters. To be sure, importers will see an additional burden. However, with oil prices at moderate levels, the increase in the import bill would be manageable at a time when India’s current account deficit is comfortable. The country closed fiscal 2016 with a current account deficit of 1.1 percent of GDP.

Rupee Weakness Doesn’t Stand Out

The second reason to be comfortable with a weaker rupee is the fact that other emerging market currencies have depreciated as much. In particular, the rupee has kept pace with peer-currencies like the Chinese yuan.

What’s leading all these currencies lower is the US dollar. The Dollar Index hit 14-year highs overnight with markets factoring in the near-certainty of an interest rate hike from US Federal Reserve.

Enough Firepower In The Form Of Reserves

Another source of comfort for the currency markets comes from the level of foreign exchange reserves. India’s forex reserves are at a comfortable $367 billion, adequate to cover more than ten months of imports. Some decline in the reserves is likely by the end of this month as the redemption of foreign currency non-resident deposits is completed. About $20 billion in deposits are expected to be extinguished between September and November, with about $7-8 billion due for redemption in the last fortnight of November.

The forex reserves, however, are adequate to cover from the redemptions while also allowing the RBI to intervene through dollar sales if foreign outflows pick-up ahead of the Federal Reserve meeting in December.

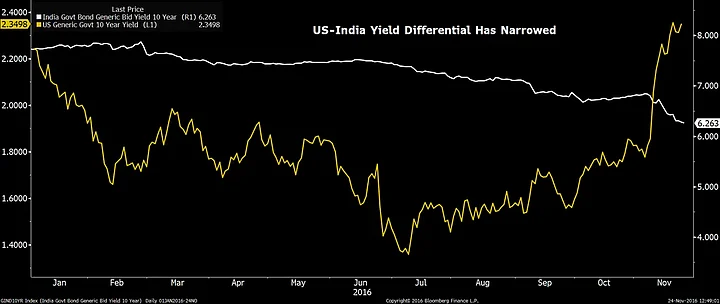

Caution On Declining Bond Yields

One point of caution, however, is the narrowing differential between US and Indian bond yields. While US bond yields have surged ahead of the expected rate hike from the Fed, Indian bond yields have plunged, following the government’s decision to withdraw Rs 500 and Rs 1,000 notes.

Over the course of this year, the differential has narrowed from 6 percentage points in July to 4 percentage points now. A narrower differential in yields makes it less attractive for foreign investors to invest in Indian government bonds. This has reflected in the $1.8 billion in outflows from the Indian debt markets so far this month.

(This article was first published in BloombergQuint)

(At The Quint, we are answerable only to our audience. Play an active role in shaping our journalism by becoming a member. Because the truth is worth it.)