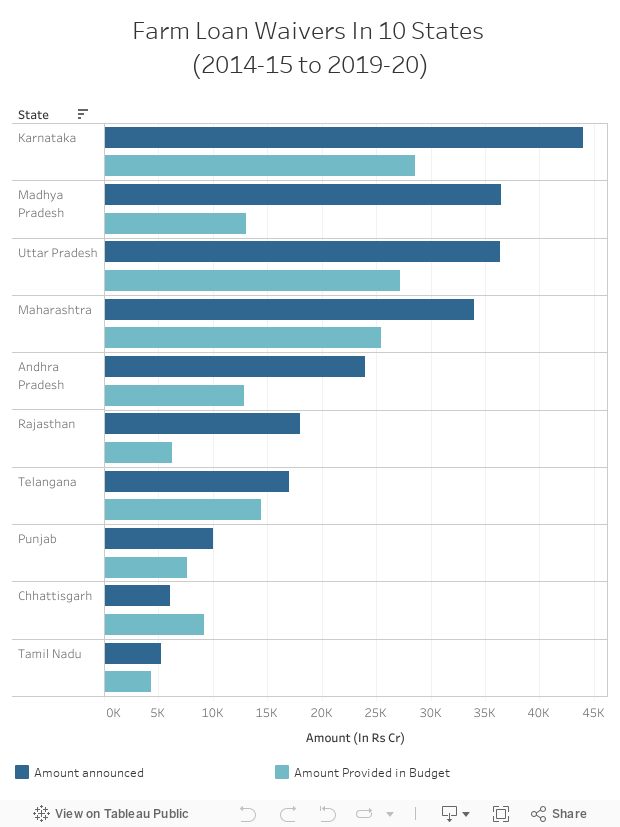

In six years to 2019-20, 10 states have announced farm loan waivers totaling Rs 2.4 lakh crore--which amounts to four times the 2019-20 budget for the rural jobs programme, or 9% of the 2019-20 Union budget--as per a September 2019 report on agricultural credit by the Reserve Bank of India (RBI).

In these six years, the year 2017-18 saw the most waivers, reaching 12% of the gross fiscal deficit (total expenditure in excess of income) in seven of these states--Andhra Pradesh, Telangana, Tamil Nadu, Maharashtra, Uttar Pradesh, Punjab and Karnataka. Altogether, they provided nearly Rs 49,000 crore in their respective budgets for loan waivers during 2017-18.

While loan waivers for highly indebted farm households can “free up lines of credit enabling them to make new investments”, the waivers “do impact the credit flow to agriculture” and create a “moral hazard” whereby borrowers default strategically in anticipation of a loan waiver, regardless of whether they will benefit from the waiver or not, noted the internal working group.

As a result, non-performing asset (NPA) levels in states that announced loan waivers showed an increase, while most other states either showed a decrease or no change.

The internal working group was created to understand the reasons for regional disparity in agricultural credit, and to suggest workable solutions.

It recommended that centre and state governments must evaluate the “effectiveness of current subsidy policies” for agri inputs and credit to make agriculture a viable and sustainable sector.

Extent of Waivers

Farm loans are justified “on social welfare grounds with the Government citing urban-rural divide in growth, social unrest and farmers' suicides as the justifications for the national ADWDRS [Agricultural Debt Waiver and Debt Relief Scheme, 2008] programme,” the report said.

The loan waivers in the six years are 24 times the Rs 10,000 crore waived by the Centre in 1990 (Rs 50,600 crore at 2016-17 prices using the GDP deflator) and nearly five times (Rs 52,500 crore) the loans waived in 2007-08 (or Rs 81,200 crore at 2016-17 prices using the GDP deflator), the study noted.

In the six years to 2019-20, nearly 64% or Rs 1.5 lakh crore has been allocated in the 10 state governments’ budgets for waivers. In 2017-18, this accounted for nearly 12% of seven state governments’ gross fiscal deficit. The deficit dropped by 4.2 and 5.3 percentage points in 2018-19 and 2019-20, respectively.

The increase in the share of farm loan waiver in a state’s expenditure “could potentially depress the state governments’ capital expenditure in agriculture” and “the deferment of budgetary provisions to meet the expenditure towards the announced loan waivers result [in an] increase in NPA levels”, the report noted.

Nearly 41% of the Rs 2.4 lakh crore waived was in 2017-18, including in Punjab, Maharashtra, Karnataka and Uttar Pradesh.

Low Farm Incomes

Agricultural and rural distress have peaked in the Indian economy in recent years, with farmers staging massive protests to demand better and remunerative farm prices. One of the promises made by the ruling Bharatiya Janata Party was to double farm incomes by 2022.

“Like loan waiver, this [doubling farm income] might also take the easier route of direct payments as already witnessed in some states,” Seema Purushothaman, faculty at the school of development in Azim Premji University and an expert on agriculture, told IndiaSpend.

“Addressing the availability of land for cultivation itself could address the issue in many parts of the country.”Seema Purushothaman, faculty at Azim Premji University

As for farm prices, they depend at least partly on the Centre’s approach in international trade and politics, Purushothaman said. By the time small landholders make cropping changes in response to trends in global trade, markets have entered newer cycles.

Indebtedness And Distress

Nearly 70% of India’s 90 million agricultural households spend more than they earn on average each month, pushing them towards debt, a primary reason in more than half of all suicides by farmers nationwide.

Low levels of absolute income and disparity between farmers and non-agriculture workers is a factor in the emergence of agriculture distress, noted a March 2017 NITI Aayog study.

Farm income per cultivator was 34% of the income of a non-agriculture worker in the early 1980s, which fell to 25% in a decade to 1993-94, the study noted. Although there was a slight improvement in the eight years to 2011-12, it showed “no change over the 1983-84 level”.

Further, real income per cultivator grew 3.4% per year in over two decades to 2015-16, but for doubling farmers’ real income (income adjusted for inflation) over the base year of 2015-16, farm incomes would have to grow annually at 10.41%, the NITI Aayog study noted.

By contrast, farm income growth for the October-December 2018 quarter was the lowest in 14 years, The Indian Express reported on March 3, 2019, at 2.04%.

Although income mobility improved country-wide in the seven years to 2012, the progress was unequal between states, and the likelihood of children pursuing the same occupation as their fathers declined for those employed in the low-productivity agricultural sector, IndiaSpend reported on July 18, 2019.

While average monthly expenditure for all households in rural India was Rs 6,646, agricultural households--that is, households that received value of produce in excess of Rs 5,000 from agricultural activities--reported 15% more expenses compared to non-agricultural households (Rs 6,187), IndiaSpend reported on September 24, 2019, based on the All India Rural Financial Inclusion Survey 2016-17.

Non-performing Assets Increase

While most states that did not announce farm loan waivers have “shown either no material change in their NPA level or have actually registered a decline between 2016-17 and 2017-18” (with the exception of Bihar, Odisha and Haryana), the NPA levels of all states that announced farm loan waivers in 2017-18 and 2018-19 went up.

The RBI described this as a “moral hazard”, suggesting that loan waivers encourage defaults among beneficiaries and non-beneficiaries.

However, farmer rights activists and researchers draw a parallel with corporate loan waivers, suggesting that farmers are unfairly singled out. The entire agriculture sector owed the banking system the same amount (Rs 7.7 lakh crore) as borrowed by the top 10 Indian corporate borrowers, IndiaSpend reported on February 18, 2019.

“NPAs may have increased because the states have written off farmer loans, but I wonder why the RBI does not say the same of the corporate NPAs?”Devinder Sharma, Agricultural expert

The RBI should refine its approach, and should not make state governments responsible for waivers, Sharma said. There should be a uniform policy where, like the corporate write-offs, farm loan waivers should also be a responsibility of the bank.

Kerala’s Loan-to-Output Ratio Three Times National Average

The all-India average loan-to-output ratio--the value added compared to the agriculture loan provided--was 0.32. Eleven states’ ratios were higher, with Kerala’s being the highest at 0.90 and West Bengal’s the lowest at 0.09.

Although Rajasthan, Bihar and Uttar Pradesh have a ratio above the national average, they do not receive enough credit for crop input requirements, possibly “due to higher share of low value crops in their overall crop output”.

Further, agricultural credit in Kerala and Tamil Nadu was nearly 180% of the states’ agriculture gross domestic product in 2015, 2016 and 2017, “indicating the possibility of diversion of credit for non-agricultural purposes”.

“There are people who avail crop loans or agriculture gold loans at special interest rates just by producing the land ownership documents, though the concerned piece of land may either be cultivated by someone else or may be lying fallow.”Seema Purushothaman, faculty at Azim Premji University

Analysts have previously commented on the diversion of farm loans towards large corporates that have interests in agri-business, as in this May 26, 2019 report in The Hindu, which pointed out that farm credits were increasingly cornered by agri-businesses, away from actual cultivators, between 2000 and 2007 in Maharashtra.

“The number of loans of less than Rs 50,000 are slashed by 50%, while the number of loans of over Rs10 crore to Rs 25 crore doubled or even trebled,” P Sainath, founder editor of People’s Archive of Rural India, wrote.

(This story was first published on IndiaSpend and has been republished with permission.)